Hydrogen: Essential Tool or Expensive Detour

Sorting climate value from industrial ambition

Hydrogen has become one of the most contested technologies in climate policy. Governments describe it as critical for net zero.[1] Industry groups present it as a transformative clean fuel. Critics argue it is inefficient, costly, and risks prolonging fossil fuel dependence.

Recent evidence has sharpened the sceptics’ case. The UK’s first hydrogen allocation round awarded just 125 MW of capacity — half the 250 MW on offer. The second round, targeting 875 MW, shortlisted projects representing only around 765 MW, and the results took nearly a year longer than expected. Against a government target of 5 GW by 2030, later revised to 10 GW, the gap between ambition and delivery is already striking.

So which is it? The answer depends on two things: how hydrogen is produced and where it is used. Today, less than 1% of hydrogen is produced with low-emissions technologies and even clean hydrogen is not a universal solution - valuable in sectors electrification cannot reach, but redundant in those it can.

Where Hydrogen Is Used Today

Hydrogen is not new. Global production reached almost 100 million tonnes in 2024 - enough to account for roughly 2.5% of global energy consumption, comparable to the entire energy demand of Germany.[2]

The largest use is ammonia production. Through the Haber–Bosch process, hydrogen reacts with nitrogen to produce ammonia, which underpins global fertiliser production. Roughly half of global hydrogen demand serves this sector. Modern agriculture would not function without it.

The second major use is oil refining. Hydrogen is used in hydrocracking and desulphurisation to remove sulphur and upgrade heavy crude into lighter fuels. Hydrogen is also used in methanol and other chemical processes.

In short, hydrogen is already deeply embedded in industrial chemistry, but not yet in a clean energy system.

Where Hydrogen Could Play a Role in the Energy Transition

The case for hydrogen strengthens in sectors where electrification is difficult, inefficient, or technically infeasible.

Steel Production

Steelmaking is one of the hardest sectors to decarbonise, since electrification cannot replace the core chemical reduction process. Traditional blast furnaces rely on coal both as a fuel and as a reducing agent to remove oxygen from iron ore. Hydrogen can replace coal in Direct Reduced Iron (DRI) processes, producing water vapour instead of carbon dioxide.

The main competing technology is carbon capture and storage (CCS) applied to conventional steelmaking. While CCS can reduce emissions, it does not eliminate them entirely and requires substantial CO₂ transport and storage infrastructure.

Hydrogen is therefore one of the few credible long-term options for steel production. It is currently 50-140% more expensive than traditional blast furnaces, depending on the region and energy cost.[3] Projections suggest that at a carbon price of around €170/tonne, green steel could actually undercut conventional blast furnace production in the EU by 2040.[4]

Industrial Heat

Beyond steel, some industrial processes require temperatures above 1,000°C — cement kilns, glass furnaces, ceramics — where hydrogen could replace natural gas as a fuel rather than, as in steelmaking, as a chemical reducing agent. Electrification is possible in some of these applications but not universally, and CCS applied to fossil fuels remains a competing pathway. Unlike steel, where hydrogen’s role is well-defined, the economics here are genuinely uncertain, and the case will vary significantly by industry and region.

Heavy Transport: Trucks, Shipping, Aviation

In transport, energy density becomes critical: a vehicle must carry its own fuel, so the weight and volume of that fuel directly affects how far it can travel and how much cargo it can carry. Batteries store energy efficiently but are heavy — a large electric truck battery can weigh several tonnes. Hydrogen contains far more energy per kilogram than a battery of equivalent weight, which is why it may have a genuine advantage in modes of transport where payload and range matter most.[5]

● For long-haul trucking, hydrogen fuel cells may compete with battery-electric vehicles where range and refuelling time are decisive.

● In shipping, hydrogen is more likely to be used indirectly through ammonia or methanol, which are easier to store and transport. Competing technologies include advanced biofuels and synthetic fuels. Electrification is viable only for short-sea routes.

● In aviation, hydrogen may be used directly in modified aircraft or indirectly via synthetic fuels made from hydrogen and captured CO₂. Batteries are not viable for long-haul aviation due to weight constraints.

Long-Duration Energy Storage

Seasonal storage is a genuine challenge for renewable energy systems. While hydrogen can absorb excess renewable electricity through electrolysis, be stored in salt caverns, and later reconverted into electricity, this process is highly inefficient. Put one unit of renewable electricity in, and round-trip you recover only 0.25 to 0.40 units as usable energy from hydrogen, compared to 0.70 to 0.90 units from a battery.[6] Pumped hydro — the other major large-scale storage technology — achieves similar efficiency to batteries, at around 75%.[7] Hydrogen therefore makes sense primarily for seasonal or very long-duration storage, where the sheer scale of capacity required makes batteries and pumped hydro prohibitively expensive.

Buildings: Heating and Cooking

Hydrogen for home heating has been heavily debated, particularly in the UK, where many homes currently rely on natural gas boilers. One proposal is to convert existing gas networks to carry hydrogen. In practice, this is more complex than it sounds: hydrogen causes embrittlement in certain metals, meaning existing pipework and fittings would require substantial replacement or upgrade. Blending hydrogen into the gas network is possible, but only up to a limited concentration — beyond that, the integrity of the infrastructure becomes a concern. Hydrogen also leaks more readily than natural gas, and cannot be odourised due to its smaller molecular size, which worsens the effective efficiency of the system and raises safety considerations.

The alternative is electrification through heat pumps. For every unit of electricity consumed, a heat pump can deliver two to four units of heat — making them two to four times more efficient than a direct electric heater, and far more so than burning hydrogen in a boiler, which loses energy at every step: electrolysis, compression, transport, and combustion.

From an efficiency and cost perspective, hydrogen for residential heating is likely a policy mistake in most contexts. Electrification is almost always superior.

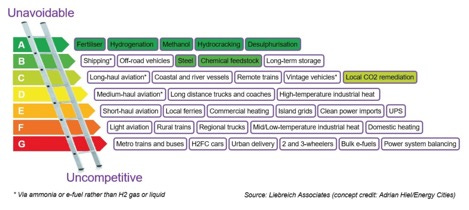

The Efficiency Principle: The Hydrogen Ladder

At the core of the hydrogen debate lies a simple thermodynamic fact: converting electricity into hydrogen and back into useful energy wastes a substantial share of the original input.

Electricity used directly in batteries retains most of its energy. Electricity converted into hydrogen loses energy at every step: electrolysis, compression or liquefaction, transport, and reconversion.

This gives rise to what analysts call the “hydrogen ladder.” Hydrogen should be reserved for applications at the top of the ladder — those where electrification is not feasible. Using hydrogen where direct electricity works well increases system costs and renewable capacity requirements.

The Hydrogen Rainbow

If the ladder is not colourful enough for you, production processes for hydrogen have over time developed their own rainbow of terms.

There are three main technologies for producing hydrogen:

● Grey hydrogen is produced from natural gas via steam methane reforming or autothermal reforming and has high emissions.

● Blue hydrogen uses similar fossil-based processes but adds carbon capture and storage. Its climate performance depends critically on capture rates and methane leakage.[8]

● Green hydrogen is produced by electrolysing water using renewable electricity. If powered by additional renewables, it has very low lifecycle emissions.

There are other, less utilised technologies too:

● Turquoise hydrogen relies on methane pyrolysis, producing solid carbon that does not enter the atmosphere instead of emitted CO₂. It remains in the pilot stage.

● Pink hydrogen uses nuclear electricity for electrolysis.

● Black or brown hydrogen is produced from coal gasification and has very high emissions.

● White hydrogen refers to naturally occurring geological hydrogen deposits, still at an experimental stage.

The climate value of hydrogen therefore depends on which colour is deployed. The preferred production route varies by region: electrolysis is more attractive in regions with abundant low-cost renewable electricity, while hydrogen from fossil fuels with carbon capture is more competitive where natural gas is cheap and storage is available.[9]

A less-discussed constraint is the electrolyzer technology required to produce hydrogen at scale. There are two main types. Alkaline electrolyzers are cheaper and don’t rely on scarce materials, but they operate best at steady loads — they ramp slowly and struggle with the fluctuating output of wind and solar, making them a poor match for the renewable electricity that green hydrogen requires. PEM (proton exchange membrane) electrolyzers handle variable power much better, ramping from zero to full capacity in seconds. But they rely on iridium, one of the rarest metals on earth. Current PEM electrolyzers use roughly 0.4–1.0 grams of iridium per kilowatt of capacity, against a global annual production of just 7–8 tonnes. Building even 100 GW of PEM capacity — a fraction of what a serious hydrogen economy would require — could consume somewhere between five and fifteen years of total world iridium supply. Reducing iridium intensity per kilowatt is an active area of research, but remains an unsolved problem at scale.

Policy Instruments and International Approaches

Hydrogen policy is, at its core, an attempt to solve a simple economic problem: low-emissions hydrogen remains significantly more expensive than fossil-based alternatives. Bridging this gap requires either raising the cost of emitting carbon or lowering the cost and risk of producing clean hydrogen.

In practice, governments have overwhelmingly chosen the latter. Public support for hydrogen has expanded rapidly in recent years, reaching around USD 38 billion globally, although this remains heavily concentrated in advanced economies and has declined from earlier expectations as projects face delays and cancellations.[10] Most current policies focus on subsidising supply rather than creating demand, reflecting both political constraints and the early-stage nature of hydrogen markets.

Three approaches to supporting hydrogen

Across jurisdictions, three broad policy models have emerged.

1. Output-Based Subsidies: Rewarding Production

The United States has adopted a production tax credit under the Inflation Reduction Act, offering up to $3 per kilogram for green hydrogen. This approach is simple and scalable: producers receive support for each unit of hydrogen produced, with stronger incentives for lower-carbon output.

The advantage is flexibility. Projects can proceed without centralised price-setting, and competition emerges naturally. However, market risk remains with producers, and fiscal costs are uncertain.[11] The effectiveness of the system also depends critically on how lifecycle emissions are measured. Weak rules risk subsidising hydrogen that delivers limited climate benefits.

2. Competitive Auctions: Price Discovery

The European Union has taken a more centralised approach through the Hydrogen Bank, which is funded by the Emissions Trading System (see my article on this here).

Under this approach, producers bid for a fixed premium per kilogram, with contracts awarded through auctions. This introduces price competition, helping to reveal the minimum subsidy required to support projects.

Early auction results suggest that support levels can fall below €0.50 per kilogram, significantly lower than earlier expectations. In more recent auctions, awarded projects represented bids ranging from €0.33 to €1.88.

At the same time, the EU has imposed strict rules on additionality and temporal matching to ensure that renewable hydrogen is genuinely low-carbon (see more on this below). These constraints improve environmental integrity but can increase costs and slow deployment.

This model prioritises cost discipline and credibility, but may limit early scale if projects struggle to meet stringent requirements.

3. Revenue Stabilisation: Reducing Investor Risk

The United Kingdom has focused on reducing risk through a Contracts for Difference-style mechanism. Producers are guaranteed a fixed strike price, covering both operating costs and a portion of capital expenditure.

This significantly lowers financing risk and may accelerate early investment. However, because strike prices are negotiated and include capital cost support, the fiscal cost per kilogram appears higher than in the US or EU models.

The UK government estimated that between 2023 and 2032 hydrogen could reduce emissions by around 41 MtCO₂e.[12] However, early allocation rounds have supported relatively small volumes, for example, around 125 MW of capacity compared to a 5GW 2030 target, highlighting the gap between ambition and deployment.[13]

A Common Pattern: Supply First, Demand Later

Despite these differences, a clear pattern emerges. Governments are prioritising hydrogen production, while demand-side policies remain limited. Globally, policy support for supply exceeds support for demand, with roughly USD 1.5 directed to production for every USD 1 targeting demand creation.[14]

This creates a risk of imbalance. Governments are targeting 27–33 million tonnes of low-emissions hydrogen production by 2030, while existing policies are expected to generate demand for only around 6 million tonnes, or up to 9.5 million tonnes including stated targets.[15] The result is a classic coordination problem: supply is being subsidised, but demand remains uncertain.

An alternative approach would be to raise carbon prices or impose stronger regulatory mandates, allowing hydrogen to compete without direct fiscal support. In theory, this would shift the burden from taxpayers to emitters. In practice, however, constraints go beyond political will.[16] Investors in capital-intensive hydrogen projects may also require long-term revenue certainty that a carbon price, however high, cannot reliably provide.

Climate or Industrial Policy?

Hydrogen policy often serves dual objectives: reducing emissions and supporting domestic industry. The UK’s Hydrogen Strategy, for example, explicitly aims to reduce investor risk and support regional development alongside emissions goals - illustrating how climate and industrial strategy are increasingly intertwined.

This is not inherently problematic, but it introduces trade-offs that deserve transparency. Supporting domestic production may come at higher cost than importing hydrogen or hydrogen-based fuels from regions with cheaper energy. Policies designed to accelerate deployment may prioritise industrial development over cost-effective decarbonisation. Taxpayers should understand whether they are funding emissions reductions, industrial development, or both.

One way to impose discipline is to benchmark hydrogen support against the cost of abatement - that is, the cost of avoiding one tonne of CO2 through a given intervention. The UK government already publishes such estimates: its central value of greenhouse gas emissions for policy appraisal stood at around £260 per tonne of CO2 equivalent in 2025. Hydrogen subsidies should be held to this standard. Where the implied cost of abatement exceeds this benchmark, the case for public support weakens considerably - and on current evidence, many hydrogen applications are likely to fall on the wrong side of that line.

Being explicit about these objectives is essential. Without clarity, and disciplined cost-of-abatement benchmarking, there is a risk that hydrogen policy delivers neither efficient emissions reductions nor competitive industries.

Green in Name Only: Why Standards Matter

Whether any of these policy models deliver genuine climate benefits depends critically on the standards used to measure them. Green hydrogen is only truly low-carbon if the electricity used to produce it is both renewable and additional. If electrolysers draw on existing renewable capacity, they can displace clean power from the grid, forcing fossil fuel plants to run more often. In that case, even green hydrogen production may increase overall emissions.

This is why the European Union has introduced strict rules on additionality, as well as temporal and geographic matching between renewable generation and hydrogen production. These requirements are designed to ensure that green hydrogen reflects genuinely new clean electricity supply.

Other jurisdictions have taken a more flexible approach. In the United States, eligibility for production tax credits under the Inflation Reduction Act depends on lifecycle emissions thresholds, but detailed rules on additionality and temporal matching have been slower to emerge and remain subject to regulatory interpretation. This creates a trade-off between faster deployment and stricter environmental integrity.

The United Kingdom has adopted a different model, combining lifecycle emissions thresholds with technology-specific requirements. Its low-carbon hydrogen standard (20 gCO₂e/MJ) requires very high carbon capture rates (typically above 95%) and tight limits on methane leakage for blue hydrogen to qualify for support. While this provides clarity, such thresholds may prove challenging to meet consistently at scale.

Blue hydrogen raises a distinct set of concerns. Its climate performance depends critically on methane leakage in upstream gas production and the efficiency of carbon capture. Small changes in assumptions, particularly whether methane is evaluated over a 20-year or 100-year global warming potential, can significantly alter estimated emissions. Under weak standards, blue hydrogen may deliver only marginal improvements over unabated fossil fuels.

From an economic perspective, these details are not secondary. Hydrogen subsidies are typically linked to carbon intensity, meaning that measurement rules directly determine which projects receive support and at what level. Poorly designed standards risk misallocating public funds and locking in high-emissions infrastructure.

For these reasons, robust carbon intensity standards and transparent lifecycle accounting are essential. Without them, hydrogen policy risks supporting technologies that fail to deliver meaningful emissions reductions.

Additional Challenges

Hydrogen is increasingly discussed as a globally traded commodity. The European Union expects to import substantial volumes from North Africa and the Middle East. However, as already noted, transporting hydrogen, whether liquefied or converted to ammonia, incurs additional energy losses.

Hydrogen’s physical properties also create engineering challenges that are more serious than they might appear. Hydrogen causes embrittlement in steel, meaning most existing gas network pipework cannot simply be repurposed - it would require substantial replacement. This matters because existing natural gas networks already leak roughly 1-3% of total throughput. Hydrogen, with its small molecular size, leaks more readily through the same infrastructure, with estimates of 3-5% or higher through unmodified pipework.

This is not merely an efficiency problem. Unlike methane, hydrogen is not itself a greenhouse gas, but leaked hydrogen consumes atmospheric hydroxyl radicals that would otherwise break down methane - effectively extending methane’s atmospheric lifetime. The result is an indirect global warming effect: a 2022 UK government-commissioned study estimated hydrogen’s indirect global warming potential at roughly 11 times that of CO2 over a 100-year horizon, with some estimates putting the 20-year figure significantly higher.[17] At a leakage rate of 3-5%, a meaningful share of climate benefit of green hydrogen could be eroded in transit. Research suggests the climate benefit of green hydrogen erodes rapidly with the leakage rate: at low leakage rates (around 1%), the near-term warming impact is limited; at higher rates (10%), green hydrogen may deliver only half the climate benefit of eliminating fossil fuels over the first two decades.[18]

Electrolysis also requires water. While water use per kilogram is not extreme, large-scale production in arid regions may require desalination, adding cost and environmental considerations.

Finally, hydrogen infrastructure creates lock-in risks. Building pipelines and blue hydrogen facilities may extend natural gas extraction and CCS networks. Policy must ensure that infrastructure choices do not crowd out more efficient electrification pathways.

Takeaways

Hydrogen is not a miracle fuel. Nor is it an unviable fantasy. It is a specialised tool that should be deployed selectively.

Today’s hydrogen market remains dominated by existing industrial uses, with new clean energy applications still at a very early stage.

It could play a role in hard-to-abate industrial processes - particularly steel and ammonia production - as well as shipping fuels, and possibly seasonal storage. It is unlikely to be efficient in residential heating, where heat pumps are more efficient and less costly. Governments should prioritise strict carbon intensity standards to prevent the subsidisation of high-emissions hydrogen.

The next decade will determine whether hydrogen becomes a core pillar of net zero, or an expensive detour in the energy transition.

[1] For example, in the United Kingdom. UK Hydrogen Strategy, page 16.

[2] IEA (2025), Global Hydrogen Review, page 33; IEA (2022) Global Hydrogen Review, page 1 (energy share figure).

[3] IEA (2025), Global Hydrogen Review, page 51.

[4] Analysis by Sustainability Directory (2025), citing projected EU ETS carbon price trajectory.

[5] This is why in passenger cars, electric vehicles are already more efficient and economically competitive.

[6] Hydrogen round-trip efficiency (20–40%): Resources for the Future (2020), Decarbonized Hydrogen in the US Power and Industrial Sectors, citing IEA (2019). Note: the text uses 25–40%, which sits within the range cited across sources; some more recent estimates put the upper bound slightly higher as fuel cell technology improves. Battery round-trip efficiency (70–90%): same RFF source, citing IRENA (2017), which gives >90% for lithium-ion and 70% for longer-duration flow batteries.

[7] Pumped hydro round-trip efficiency (~75%): IRENA/IEA-ETSAP (2012), Electricity Storage Technology Brief; and International Hydropower Association (2020). Range across sources is consistently 70–85%.

[8] The choice of methane accounting horizon is particularly important: over a 20-year period, methane traps far more heat than under the standard 100-year metric, meaning even small leakage rates can materially undermine blue hydrogen’s climate advantage.

[9] IEA (2025), Global Hydrogen Review, page 51.

[10] IEA (2025), Global Hydrogen Review, page 203.

[11] Beyond fiscal cost, output-based subsidies of this kind can also create unintended distortions further up the supply chain — inflating demand and prices for scarce upstream inputs, such as iridium, in ways that are difficult to anticipate or control.

[12] UK Hydrogen Strategy (2021), page 16.

[13] DESNZ (2023), Hydrogen Production Business Model / Net Zero Hydrogen Fund: HAR1 Successful Projects, 14 December 2023. The 5 GW 2030 target was set in the UK Hydrogen Strategy (2021), page 4, and subsequently revised to 10 GW.

[14] IEA (2025), Global Hydrogen Review, page 203.

[15] IEA (2025), Global Hydrogen Review, page 203.

[16] In the EU, for instance, accelerating the removal of free carbon allowances under the ETS (the mechanism that would most directly raise the carbon cost faced by industry) would require deviating from an already-negotiated phase-out schedule. If anything, political pressure is currently running in the opposite direction.

[17] Warwick et al. (2022), Atmospheric Implications of Increased Hydrogen Use, commissioned by BEIS, University of Cambridge / National Centre for Atmospheric Sciences, University of Reading.

[18] Ocko, I.B. and Hamburg, S.P. (2022), Climate consequences of hydrogen emissions, Atmospheric Chemistry and Physics, 22, 9349–9368. The leakage rate estimates used in this analysis draw on Frazer-Nash Consultancy (2022), Fugitive Hydrogen Emissions in a Future Hydrogen Economy, commissioned by BEIS.