Optimisation vs. Stabilisation: Why Climate Policy Looks Different Across Regions

Fighting the climate battle on two fronts

A couple of months ago, while preparing an economic outlook on Southeast Asia, I was constantly brought back to the same realisation: climate policy changes shape as sharply as the regions it is applied to. In much of Southeast Asia, climate shocks are not rare disruptions but recurring macroeconomic events. Empirical evidence supports this: severe natural disasters in developing Asian economies can reduce per capita GDP by as much as 6–7% on impact, with effects that can persist for years. The importance of climate policy in the region rests on long-term carbon goals just as much as short term disaster resilience.

In the most climate ambitious countries in Europe, climate policy is generally framed as a long-run project. Much of the focus is placed on developing renewable energy strategies and gradually increasing incentives meant to reshape investment decisions over decades. This framing makes sense in the context of relatively stable institutional and fiscal environments, where climate-related shocks, while costly, are typically absorbed without fundamentally disrupting macroeconomic policy or long-term policy commitments. In short, climate policy broadly becomes an exercise in optimisation: set the constraint, price the externality, and trust that markets and technology will adjust.

In Southeast Asia however, climate policy is fighting a battle on two fronts. Like Europe, it is addressing challenges such as expanding its energy grid and incentivising green technological advancement: the long-run project. Yet, as Southeast Asia is one of the most disaster-prone regions on earth, these policies must coexist with intensifying typhoons, flooding, extreme rainfall, and droughts. Emerging economies in Southeast Asia face approximately 100 disasters per year (almost one every 3 days!), affecting roughly 80 million people and with total costs upwards of 700 billion USD over 2010-2025. As a result, climate change extends beyond a long-term environmental issue into a regular source of potentially macroeconomic stress that tests institutional and economic resilience. In this environment, the challenge expands beyond designing climate policy, but ensuring economies stay resilient when the next shock hits.

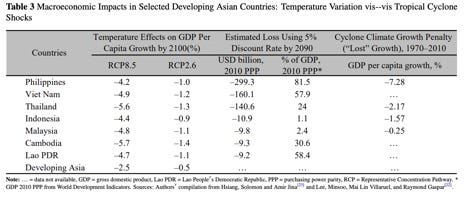

Indeed, empirical estimates such as those in the table below suggest that repeated cyclone exposure reduced cumulative GDP per capita growth in the Philippines by over 7% between 1970 and 2010. Forward-looking projections estimate cyclone-related losses equivalent to more than 80% of 2010 GDP (discounted to 2090), alongside additional substantial losses across several Southeast Asian economies.

Source: (Lee, Alano & Villaruel, 2020).

Mitigation, Adaptation, and Binding Constraints

Climate policy is often divided into two categories: mitigation and adaptation. Mitigation reduces emissions to limit future climate change while adaptation confronts the physical impacts of climate change that are already occurring.

In relatively stable macroeconomic environments, mitigation naturally dominates. Carbon pricing, emissions trading systems, and renewable energy deployment are long-run tools designed to shape investment decisions over decades. Their effectiveness depends on policy credibility and institutional stability.

In highly disaster-exposed economies, adaptation is not secondary. It is macroeconomic stabilisation. Flood defences, resilient infrastructure, agricultural insurance, and disaster risk financing determine whether climate shocks become fiscal crises such as inflation spikes or debt stress.

The difference, then, is not climate ambition. It is whether macroeconomic stabilisation is already institutionalised or must be built alongside decarbonisation. Climate ambition is not the dividing line - stability is.

Europe and Climate Policy as Planning

Climate ambitious European countries’ climate policy operates in a very structured way. Long-term objectives serve as anchors for expectations regarding future climate action. These anchors can take different forms: model-based valuations such as the social cost of carbon or science-based constraints such as carbon budgets. Tools such as the European Emissions Trading Scheme (EU ETS) and the way it prices carbon are designed to function continuously and predictably, and although they are revised and updated from time to time, their purpose is to establish a framework in which governments can commit to forward-looking objectives reliably.

Recent climate-related disasters demonstrate how this framework operates under stress. In July 2021, severe flooding in Germany and Belgium caused over €40 billion in damage. While substantial in absolute terms, these losses amounted to well under 2% of Germany’s national GDP and were spread over several years of reconstruction.

Governments mobilised reconstruction funds and insurance payouts to address the damages. Roughly a quarter to a third of the economic losses were insured, which is far from full coverage, but significantly higher than in many parts of Southeast Asia, where flood insurance penetration in many countries is often low single digits. The remaining costs were financed through existing fiscal frameworks supported by Germany’s robust institutions, without triggering a systemic macroeconomic crisis.

This reflects a broader structural reality. European economies operate with deeper financial systems, credible and robust institutions, and relatively higher insurance coverage. Climate-related disasters occur, but they do not dominate annual macroeconomic decision-making. As a result, stabilisation capacity largely precedes climate optimisation. Europe’s climate policy can therefore function primarily as a long-run planning exercise with little fear of climate related macroeconomic shocks.

Southeast Asia and Climate Policy as Repeated Emergency

The policy environment in Southeast Asia is fundamentally different. The frequency of climate related disasters is high enough that they influence annual fiscal and macroeconomic decision making, with around 86 billion USD lost annually to disasters. In many emerging Asian economies, more than 90% of disaster losses remain uninsured, creating large direct burdens on households and government balance sheets. The need to respond to emergencies and rebuild infrastructure competes with long-term climate investment and development objectives. For many economies in the region, climate-related shocks translate into macroeconomic stress through sudden fiscal pressure and inflation volatility. As an example, let’s look at the Philippines where, in late 2022, typhoon-related damage to agriculture led to a surge in food prices and pushed inflation to 7.7 percent, the highest level since 2008: a macroeconomically meaningful shock.

Under these conditions, it can be more difficult to stabilise climate policy. Long-term mitigation and economic strategies must be built resilient as they will continually be tested by short term needs. An extra dimension is added when exposure also changes the cost structure of climate policy. Adaptation is often more expensive in disaster-prone, tropical economies because infrastructure must be built to withstand repeated shocks. Climate policy must therefore operate as both transformation and stabilisation.

It is here that the temptation to “borrow” European style climate policy often runs into problems. Tools that depend on consistent commitments and predictable implementation experience difficulties in an environment where the next crisis is always just around the corner. The issue is not that such tools are inappropriate, but that they must be embedded within a stronger stabilisation framework. Building economies that can withstand shocks becomes just as important as advancements in climate policy.

When Disasters Stop Being Macroeconomic Events

The implications of this difference can be illustrated by examining the example of Japan, which occupies an intermediate position between Europe and much of Southeast Asia, as it shares many of the same disaster risks as Southeast Asia including typhoons, flooding, extreme rainfall, and periodic droughts, yet, importantly, like Europe, Japan has maintained its broad macroeconomic stability along with long-term energy and climate strategy.

Japan’s disasters are not smaller or less painful than those in Southeast Asia. Instead, Japan’s disasters are more economically predictable and are absorbed through institutions built to manage disaster risk. While costly, shocks are typically not systemic and inflationary impacts are contained due to the quality of institutions in place.[1]

An example can be seen in the 2019 Typhoon Hagibis which caused flood damage estimated at about 2.1 trillion yen (~0.75 % of GDP) and contributed to a sharp contraction in output in the final quarter of the year. The economic impact was real. However, the shocks did not trigger a fiscal crisis. Reconstruction was financed through existing institutional frameworks, and insurance coverage absorbed a significant portion of the losses. Deep capital markets and strong fiscal capacity allowed Japan to fund reconstruction at low cost, limiting long-term macroeconomic scars.

Japan therefore illustrates an important principle: high disaster exposure does not necessarily translate into macroeconomic instability. Once stabilisation capacity is institutionalised, climate policy can operate alongside recurring physical shocks.

Different Operating Conditions

All of this to say, Southeast Asia is addressing a different element of the climate challenge. Europe can focus on optimising its emissions reduction pathway over time, whereas much of Southeast Asia must ensure that its economy remains viable in the face of frequent disaster shocks, which are more likely to become significant at a macro level when stabilisation capacity is weaker.

While Southeast Asia is actively pursuing mitigation efforts (including increased renewable energy development, grid upgrades and deployment of clean technologies) there is an ongoing need for adaptation and stabilisation.

The implication is not that Southeast Asia should delay its pursuit of ambitious climate policy, but that climate ambitions must be protected through economic resilience to disaster shocks.

Climate Policy Under Recurrent Shock

This highlights an important structural distinction. Long-run mitigation tools (e.g., carbon pricing, emissions trading systems, binding targets) rely on stability. If policies can’t rely on macroeconomic stability in the face of crisis, then investors will not receive stable signals regarding investment opportunities. Our key takeaway is that institutions that enable governments to respond to disasters without revising their budgets provide the environment for successful mitigation efforts.

Therefore, disaster risk financing, fiscal buffers, insurance frameworks, and robust public financial management are not ancillary elements to climate policy - they are enabling infrastructure. For example, the World Bank’s Disaster Risk Financing and Insurance Program supports countries to build protection strategies to help governments meet post-disaster funding needs by combining sovereign financing, insurance, and market instruments. Moreover, Japan has played a leading role in developing disaster finance plans with the Sendai Framework for Disaster Risk Reduction which was adopted at the Third UN World Conference on Disaster Risk Reduction. Programs or strategies like these promote economic resilience and increase the probability that more robust long-term climate objectives can be planned even in the face of repeated disaster shocks.

Conclusion

The takeaway, then, is that climate policy designed for a relatively stable institutional environment cannot be transplanted wholesale into economies where shocks are frequent and fiscal space is routinely tested. Economic resilience to disasters is a whole other front that Southeast Asia must fight. We see that Southeast Asia must coincide green development goals with disaster risk reduction to ensure the macroeconomic stability needed for these long-term climate ambitions.

Institutional and fiscal resilience are not a detour from decarbonisation in Southeast Asia, but a necessary corequisite for it.

[1] While the 2011 Fukushima disaster significantly altered Japan’s energy mix and delayed its decarbonisation trajectory by shutting down much of its nuclear capacity, it did not undermine the country’s macroeconomic stability. Japan retained the fiscal and institutional capacity to finance reconstruction, invest heavily in coastal defenses such as sea walls, and continue long-term energy planning within a stable policy framework.